MODERATE GROWTH AND POSITIVE RESULTS FOR LUXURY GOODS SECTOR

The 2015 Altagamma Observatory, the annual snapshot of the performance of the luxury goods industry, takes stock of the health of the sector: despite currency headwinds and consumption shrinking in some of the key geographical regions, the luxury industry continues to grow.

The luxury goods industry is proving stronger than any economic crisis and the positive trend begun in 2010, after the 2009 slowdown, continued this year. Together with the Arts sector, which this year was included for the first time in the analysis, the global luxury goods market went beyond the €1000 billion barrier in 2015.

At current exchange rates, demand for Personal Luxury goods increased by about 13%, reaching a total value of €253 billion. This strong growth will be reflected in the end of year results of European companies. In real terms, consumption is expected to grow by 2% in 2015.

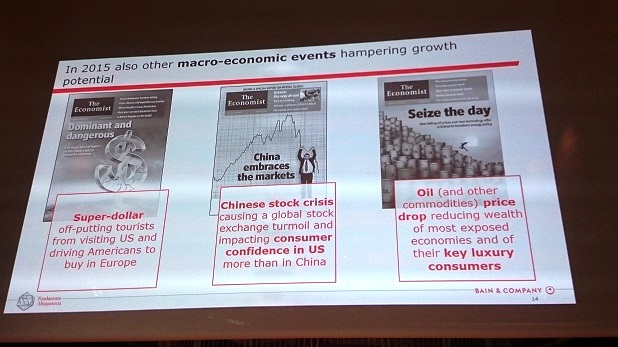

With the exception of Russia, there is good news coming from the main geographic markets, with Europe growing by 5% at a constant rate and Japan confirmed as the biggest growing market (+9%) thanks to renewed Japanese consumer confidence and tourism from China. The US is stable (0%).

The Mainland China market shrunk slightly (-2%), but China remains the dominant nation when it comes to the consumption of luxury goods with a 31% share of the world total, to the benefit mostly of Japan, Korea and Europe. With regard to sales channels, retail continued to increase its share amounting to 34% of the overall market in 2015 (+20%). Strong growth also for the online (+40%) and outlet (+35%) channels. The fastest growing product category is jewellery (+6%), seen as a safe investment by consumers all over the world, and is followed by footwear (+4%). Spending on watches was down (-6%), with the other categories recording moderate growth.

Confirming the fact that tourism flows are increasingly important to the geography of consumption, Italy boasts a substantial increase in Tax-Free Shopping (+19% with respect to 2014), but double-digit growth rates were also recorded by the main European markets, with the exception of the UK, which paid for the currency effect.

Forecasts for 2016 suggest growth consistent with the “new standard” for global consumption of high-end products, with an average increase estimated around +3 / +3.5%.

During the [highlight color=”yellow”]Round Table[/highlight] discussion that followed the presentation of the studies, the results were commented upon by Armando Branchini (Fondazione Altagamma), Claudia D’Arpizio (Bain&Company), Matteo Lunelli (Cantine Ferrari), Claudio Luti (Kartell), Vittorio Ogliengo (UniCredit), Laudomia Pucci (Emilio Pucci), Giovanni Tamburi (Tamburi Investment Partners), Francesco Trapani (Clessidra SGR) and Giovanna Vitelli (Azimut Benetti).

According to Armando Branchini, Vice Chairman of Fondazione Altagamma, “global consumption going beyond the thousand billion euro threshold represents a milestone for our industry. European companies will achieve great results this year, but moderation is required: real growth is modest and will remain so also in 2016. A situation of moderate growth demands that companies substantially reassess their investment strategies: pursue organic growth, keep a tight grip on the use of liquidity, reduce the cost of capital.”

[divider style=”dashed” top=”20″ bottom=”20″]

Altagamma Global Market Monitor. By Bain & Company

At the end of 2014, the global market was worth €224 bn, with a 3% growth at constant exchange rates. Estimates for 2015 suggest a small increase in the global consumption of luxury goods of around 1-2% at constant exchange rates and 13% at current exchange rates, for a market of an overall value of €253 billion. This growth is led mainly by the online (7% of the total) and outlet channels. The fastest-growing category was jewellery (+18% at current rates and +6% at constant rates), seen as an investment by consumers in all geographic areas. In second place was footwear (+16% at current rates and +6% at constant rates). At global level, Chinese consumers remain the fastest-growing national group (31% of the total). In terms of geographic areas, Japan stands out (+13% at current rates and +9% at constant rates), while Russia has fallen away dramatically (-25% at current rates), Europe has made progress (+9% at current rates and +5% at constant rates), the US is stagnant and the Middle East has grown slightly in real terms.

Altagamma Consensus 2016. By Fondazione Altagamma, with the contribution of leading international expert analysts.

The forecasts for 2016 suggest moderate growth for all sectors, in line with the trend towards the normalisation of the industry. Clothing +3%, Tableware +2%, Hard luxury +3%, Accessories +4%, Perfumes and cosmetics +4%. The geographic markets are also expected to grow, at constant exchange rates, with Europe (+4%) and Japan (+5%) still the best performing. North America is expected to grow around 3% with more modest the growth in Latin America (+1%). The contraction of tourism from Russia will hold back the Middle East, which was nevertheless up by 3%. EBITDA forecast for 2016: +4% on 2015.

Tax-Free Consumption in the European Union. By Global Blue.

Tax-Free Tourist Shopping boomed in Europe, recording a 26% increase in the first nine months of 2015 with respect to the same period last year. Chinese tourists were the biggest spenders (36% of the European market) and there was a comeback from the Americans (+57%), who hold a 5% market share. Italy is one of the preferred destinations for international tourists with an increase in purchases by the Chinese (+71%) making up for lower spending by the Russians (-42%, but still in second position). The impact of Expo Milan 2015 is unclear: Global Blue shows a positive trend in the whole of Europe, as if the EXPO has had a widespread effect. The Luxury segment recovered, accounting for more than 49% of the total.

Fashion & Luxury Insight. By SDA Bocconi and Altagamma.

For listed fashion and luxury companies, 2014 confirmed the positive trends with regard to sales, ROI and investments. Medium-sized companies performed best. The number of stores fell with companies focused on restructuring and optimising their networks rather than expanding them. Luxury goods remain the most profitable segment but for the first time sales (+4.5%) grew less than the average (+6.3%). The differential in terms of ROI also decreased (+15.7% against a +12.1% average). High-end companies invested more in their networks of stores (7.5% v. 3.8%).

Food & Hospitality Insight. By SDA Bocconi and Altagamma.

For public companies in the Food and Hospitality sectors there was a slight fall in turnover, equal to 0.5%, bucking the trend of previous years; nevertheless, a substantial number of companies were able to grow. Facing the reduced profitability of investments and smaller margins, the companies considered have increased their investment in organic growth and M&A, a sign of widespread confidence and the ongoing consolidation processes in the sectors.

[divider style=”dashed” top=”20″ bottom=”20″]